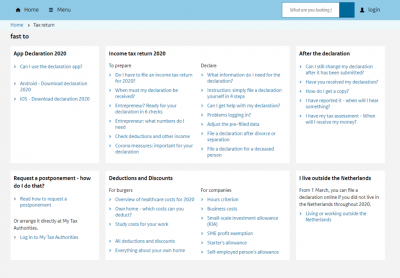

The article provides information to help you complete aangifte inkomstenbelasting or income tax return in the Netherlands.

Who has to file an income tax return?

- Everyone who receives a declaration letter from the Dutch Tax and Customs Administration (Belastingdienst) must file an income tax return.

- If you have not received a declaration letter from Belastingdienst, you may still need to file an income tax return.

That's why it's good to check whether you need to file a declaration. You may even be able to get a tax refund. For example, if you have deductible expenses such as healthcare costs, costs of various courses.

Here you can find what types of costs you can deduct: https://www.belastingdienst.nl/wps/wcm/connect/nl/aftrek-en-kortingen/aftrek-en-kortingen

You can check whether or not you need to file an income tax return by completing a test statement in Mijn Belastingdienst. However, you will need a DigiD to login to their platform. If you do not have a DigiD (a digital account that helps you to identify yourself securely to state institutions and receive the necessary information - https://www.digid.nl/en/help), then you will need to apply for one online. Also, as long as you do not submit the data (which you will choose at the end), then the declaration will not be registered. In addition, the Belastingdienst online platform is only available in Dutch, so if you have problems understanding it you can use the Google Translate function in your Chrome browser, or we advise you to ask a good Dutch speaker for help.

Once you have completed the declaration, you will see the result immediately:

- If, after completing the form, you are shown an estimated refund of €16 or more, then submit a declaration.

- Do you get less than €16 back? Then you do not need to submit a declaration. Because we don't pay amounts under €16.

- If after filling in the form it appears that you have to pay €48 or more, then you are obliged to submit a declaration.

- Is the amount payable less than €48? Then you do not have to submit a declaration.

What is the deadline for submitting the tax return?

You must complete your 2020 income tax return between 1 March and 1 May 2021. If you have requested or received a deferment, then you have more time to file your tax return, but the deadline will be communicated by Belastingdienst.

How can you complete your income tax return?

In the Netherlands, you pay income tax on your taxable earnings.

The tax authorities use your income tax return to determine your tax assessment: will you have to pay tax or receive a tax refund?

There are three different types of taxable income (the boxes you will find on your tax return) and each has its own tax rates. To calculate your taxable income, you need to aggregate your income in these three boxes:

- Box 1: Labour and property income

- Box 2: Financial interests in a company (e.g. shares)

- Box 3: Savings and investments

Write down on a piece of paper the 3 boxes and their values, as we will list them below in various possible scenarios. Also, on the Belastingdienst website you will find the 4-step guide you can follow to complete your income tax return:

It is very important that before you start filling in your tax return, you gather all the information you will need. This depends on your personal situation. Below are some examples of information that many taxpayers will need for their 2020 tax return.

- Bank accounts balance

You need a financial overview showing your bank account balances. You will need these balances from 1 January 2020 to 31 December 2020 (for box 3).

- Home mortgage situation

This is a statement of your outstanding mortgage debt and interest and other charges you have paid on your home. You will need this information for questions about your home in box 1.

- The value of your house on the valuation of real estate (WOZ-waarde)

WOZ-waarde (in Dutch) is the estimated market value of your house on 1 January of the previous year. This value is specified in the municipal tax return from your local council. For the 2020 tax return, the figure you need is the value of your house on the reference date of 1 January 2019.

- Annual statement of income from employer or pension provider

You need your 2020 annual salary or pension statement. The details you need include the amount of income tax and national insurance contributions deducted from your 2020 salary.

- A list of charitable donations

If you have made donations (for which you have a receipt) to one or more officially registered charities in 2020, we advise you to make a list of these donations. If they meet certain conditions, donations are tax deductible. Enter them first in box 1. If you still have deductible donations after the income declared in box 1 has been reduced to zero, you can claim them in box 3 and then in box 2. You must distinguish between "one-off" donations and "recurring donations". In the case of the latter, the obligation to make donations is laid down in a contract or notarial deed of gift.

If you donate to one or more public benefit organisations (known as ANBI in Dutch) that have been designated by the Tax and Customs Administration as a cultural organisation, you can increase the value of the donation by a certain percentage on your tax return. For tax purposes, you can increase the value of regular donations and other donations you have made privately to organisations of public cultural interest in 2020 by 25%, up to a maximum of €1,250. You will reach this maximum if you give at least €5,000 to organisations of public cultural interest in a calendar year.

- A list of all your medical expenses

If you incurred medical expenses in 2020 due to illness or disability, you may be able to deduct them from your taxable income under certain conditions. First in box 1 and if you have any remaining deductible medical expenses, you can declare them in box 3 and box 2. There is an income-related tax deduction threshold for medical expenses.

What should you look out for when completing your tax return? We list below the main things you need to know:

- Income tax and dividend tax

If you received dividends from Dutch companies in 2020, they will be subject to dividend tax at a rate of 15% of the gross amount. Declare any dividends received under 'te verrekenen bedragen' (compensable amounts) 'ingehouden dividendbelasting' (dividend tax withheld). You can offset the total amount of dividend tax against the income tax payable. If you do not have to pay any income tax, the Tax Administration will refund the dividend tax you have paid.

- Home loan

- Deductible property costs and interest

Any costs directly related to taking out, extending or repaying a loan for your home are deductible from your taxable income (from box 1) for the year in which these costs were incurred. These costs include advice and brokerage fees for your mortgage adviser, notary fees and land registry fees in connection with the mortgage deed, valuation costs for obtaining the mortgage and costs involved in applying the national mortgage guarantee.

- Deduction of refinancing or early repayment charges

If you incurred taxes because you refinanced or repaid the mortgage on your home in early 2020, you can deduct these taxes from your taxable income in box 1.

- Obligation to disclose information about home loans

If you borrowed money from your company, a family member or someone else to buy your home, note that you may be required to provide details of this loan on your tax return. The deduction of interest and other costs in relation to such loans is conditional, among other things, on your obligation to make repayments on the loan throughout the term of the loan. This is because the tax and customs authorities need to be able to check that you have made sufficient repayments on the loan.

- Divorce

- Ex-partner maintenance

If you pay maintenance to your former partner, the amount you pay will generally be tax deductible. The former partner must declare the same amount as taxable income on his or her income tax return. Child maintenance is not tax deductible. Nor is the obligation to pay child maintenance considered a form of debt in box 3.

- Mortgage interest deduction in case of divorce

If you have moved out of your home due to a planned or finalized divorce, while your former partner continues to live there, you will be able to continue to use the mortgage interest deduction for your share of home ownership for up to 24 months after you move out.

- Box 3

- Assets in box 3

Box 3 of the tax return is where savings and investment income is taxed. Capital declared in this box includes savings, securities, a second home and any rental property. At least the first €30,846 in capital declared in box 3 is tax-free in 2020 (partners for tax purposes: €61,692 combined) as a 'tax-free allowance'. Apart from this, there are other specific exemptions in box 3 for which you may be eligible.

Not all your assets need to be declared in box 3. Assets for your personal use or use within your family, such as your car, the contents of your home and savings under the Lifetime Savings Scheme do not have to be included in your assets in box 3.

- Lottery winnings

Any lottery winnings you have received by midnight at the beginning of 1 January 2020 or any entitlement to lottery winnings on that date from a previous draw are considered part of your Box 3 capital from that reference date. When exactly the winnings were paid into your bank account is irrelevant. For example, if you won a lottery prize at the end of 2019, you must declare it on your 2020 income tax return. Any lottery winnings in 2020 must be declared on your 2021 income tax return.

- Educational expenditure

If you took courses or were enrolled in an educational program related to your current or future profession in 2020 and incurred costs, certain amounts you paid in 2020 will be deductible as educational expenses. Enter them first in box 1 and, if you have any remaining deductible educational expenses, you can declare them in box 3 and box 2.

Deductible educational expenses include tuition fees, course fees, school fees and examination fees. However, they do not include travel expenses and the cost of a laptop, tablet or printer, etc.

- Own business

- Workspace for your business.

If you use a separate workspace in your home for business activities, such as running a limited liability company, you may be eligible for a deduction for your business. This is subject to strict rules. HM Revenue and Customs has developed a tool to assess a limited number of possible situations.

- Funds receivable and payable to your company.

If you have borrowed funds from your company, you owe the company money and therefore pay the company (business) interest.

This is a debt you must declare in box 1 or box 3.

If you are using the loan to buy, renovate or maintain your home, this loan should, in principle, be reported in Box 1 as it will then be considered home purchase debt.

If you used the loan amount to buy an asset that you subsequently made available to your company, then this loan will also be reported in box 1.

In all other cases, the debt will generally go into box 3.

If you have a current account relationship with your company with fluctuating debit and credit balances, you do not have to declare interest if the balance in this current account has not exceeded €17,500 and has not fallen below -€17,500 at any time during the year. Even then you will not have to declare any current account debt in box 3.

Please note:

- Belastingdienst focuses mainly on digital communication. Activate your online account at nlto access your messages. To use this service you must first have a DigiD.

- After filing a tax return, you will receive a preliminary assessment (voorlopige aanslag)from the tax authorities. The preliminary assessment takes between 6 and 12 weeks after the submission of the return. The preliminary assessment is simply an estimate.

After the tax authorities have verified your return, you will receive a final assessment (definitieve aanslag) together with payment or refund details.

It is also important to refer to the additional information function of each data entry field, marked by a question mark placed in a yellow square.

References:

https://www.abnamro.nl/en/personal/themes/tax-return/index.html

https://www.belastingdienst.nl/wps/wcm/connect/nl/belastingaangifte/

Author: Cristina Vrîncianu